How to Get Ready for Bigger SBA Loan Limits

In Part 1 of this series, we covered the big SBA update: as of July 4, 2026, qualified borrowers who secure an SBA 7(a) loan first may be able to access up to $5 million through the 7(a) program and up to $5 million through the 504 program, for a combined total of up to $10 million in SBA-backed financing.

Read Part 1 here: The SBA Just Raised the Ceiling. Now What?

Now comes the less sparkly part.

The SBA ceiling may be higher, but that does not mean lenders are handing out oversized checks like parade candy.

You still need a plan. You still need documentation. You still need to show the business can handle the financing. Deeply rude, yes. Also very normal.

So if you want to take advantage of the new SBA opportunity, here’s what to get ready before you fall in love with a building, business acquisition, equipment package, or expansion plan.

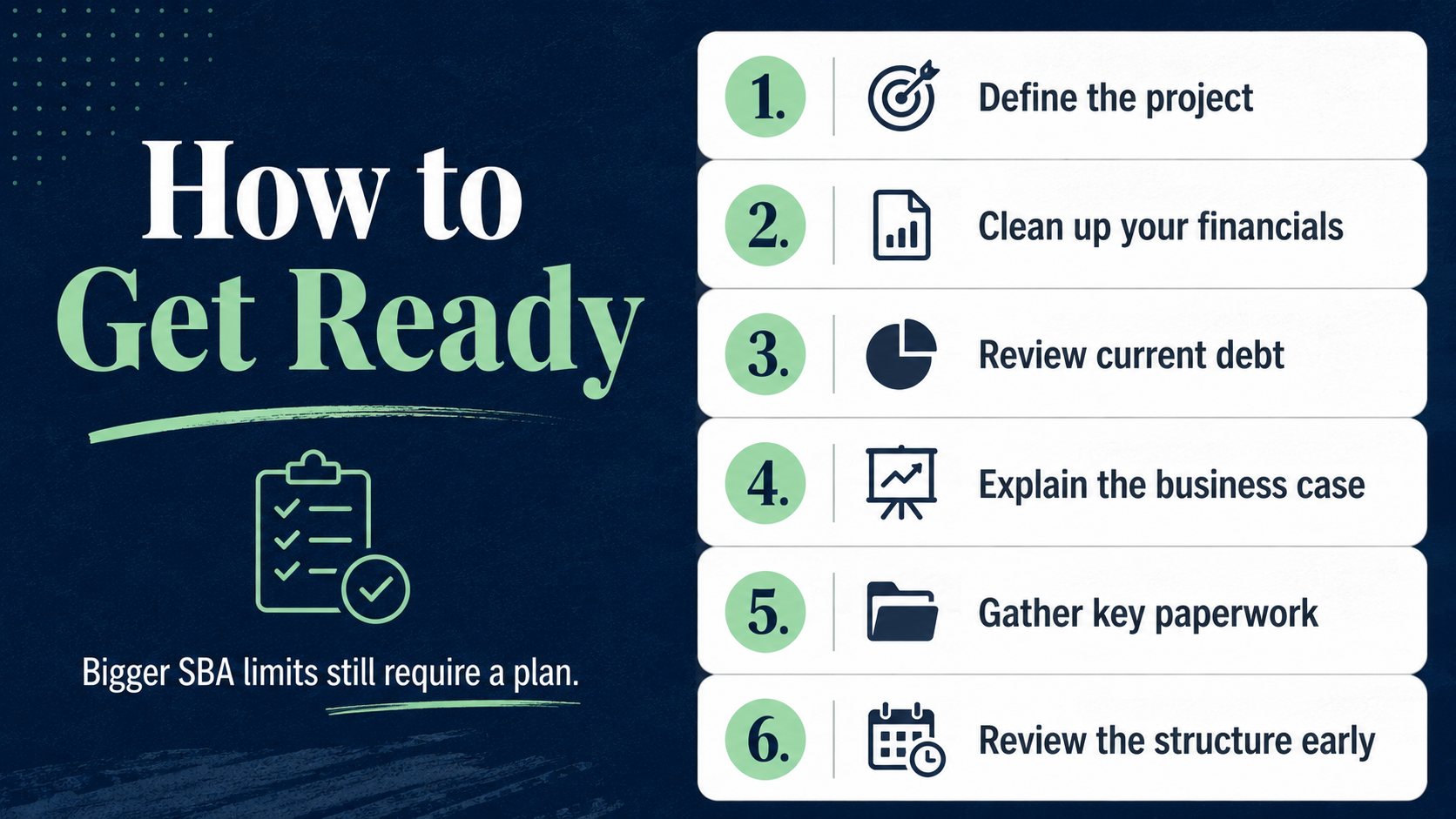

1. Know what you are actually financing

“Growth” is not a use of funds. Be specific.

Are you buying commercial real estate? Acquiring another business? Purchasing equipment? Refinancing existing business debt? Expanding a facility? Opening a new location?

The financing structure should match the move. SBA 7(a), SBA 504, or a combination of the two may make sense depending on the project.

2. Get your financials cleaned up

Your financials do not need to look fancy. They do need to make sense.

That means current profit and loss statements, balance sheets, tax returns, debt schedules, and bank statements should be organized and reasonably up to date.

If your financials require a translator, a treasure map, and three emotional support beverages, fix that before you apply.

3. Understand your current debt

Before a lender looks at giving you more capital, they are going to want to understand what debt the business already has.

Monthly payments. Balances. Interest rates. Terms. Daily or weekly repayment obligations. Lines of credit. Equipment loans. Merchant cash advances. All of it.

This matters because existing debt affects how much room the business may have for new financing.

4. Be ready to explain why the move makes sense

A lender does not just want to know what you are buying. They want to know why.

How does this purchase, acquisition, refinance, or expansion help the business?

Will it increase capacity? Lower costs? Add revenue? Improve operations? Create stability? Replace a bad debt structure?

The better you can explain the business case, the stronger the conversation.

5. Gather the basic paperwork early

Do not wait until a seller, landlord, broker, or vendor is breathing down your neck.

Start pulling the basics now:

Business tax returns

Current financial statements

Debt schedule

Ownership information

Business entity documents

Purchase agreement or letter of intent, if available

Equipment quote, if applicable

Real estate details, if applicable

Yes, paperwork is annoying. So is missing an opportunity because everything is scattered across inboxes, shoeboxes, and “I think my accountant has that.”

6. Talk through the structure before you commit

This is the big one.

Before you sign anything, get a funding review. The structure matters. The timeline matters. The use of funds matters. And the product matters.

The biggest number available is not always the smartest option.

At Credit Banc, we help business owners review SBA financing, acquisition funding, commercial real estate financing, equipment financing, refinancing options, and other structured lending solutions.

The new SBA limit may create more room for bigger moves.

But bigger moves still need smarter planning.

If you are considering an acquisition, expansion, refinance, equipment purchase, or commercial real estate project, schedule a call with Credit Banc to learn more about what may be possible.

CLICK HERE to talk SBA Financing with a Credit Banc Advisor Today